— Здесь вы сможете найти отзывы по банкам из таких городов

как Москва, Санкт-Петербург, Новгород и многих других

One common misconception on the opposite mortgage loans is that the lender has the house

Home prices have left up within nation in recent years. In case the home’s value is much more than when you initially grabbed your reverse financial, you have got alot more domestic equity you should use access.

The latest FHA increased the lending restriction having 2023 so you can more than so many cash for the first time, and that means you could possibly availableness more what was available in case your financing are originated.

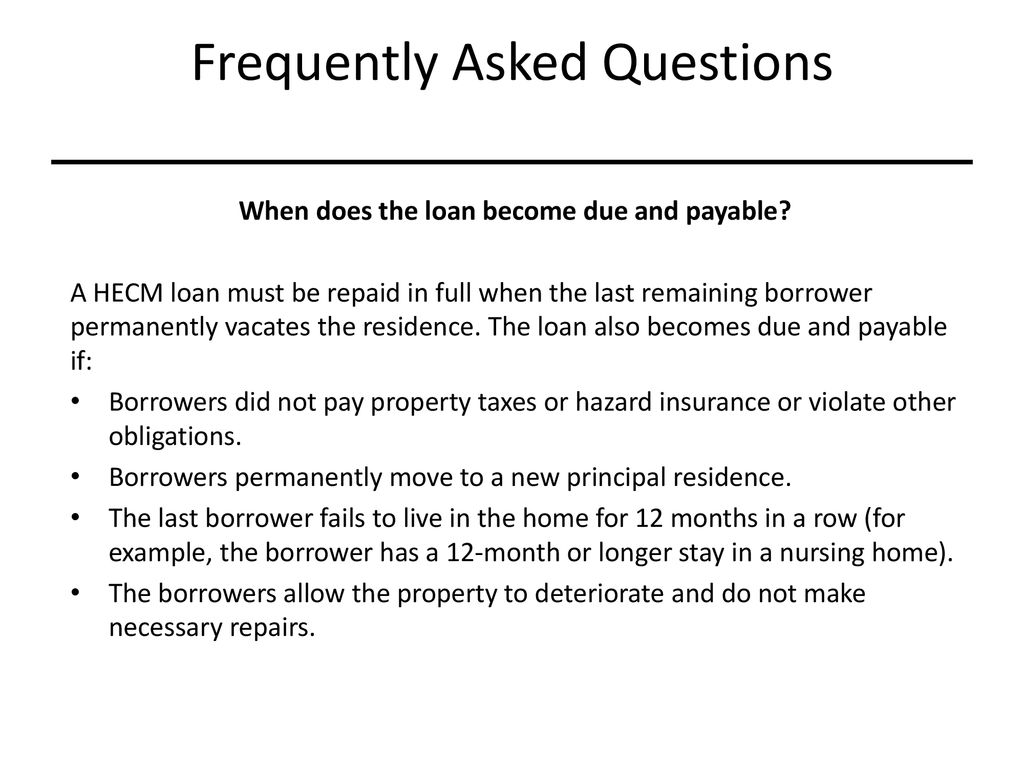

Frequently asked questions

While the a government-insured and you may federally controlled home mortgage, there are numerous extremely important conditions individuals need certainly to fulfill in order to be considered, including the following:

- You should be at least 62 yrs old.

- You need to individual your home.

- Our home need to be the majority of your quarters.

The mortgage is born and you may payable making use of the proceeds of your own product sales of the home and/or proceeds from a great refinance when the very last borrower or eligible low-borrowing from the bank partner movements out of the house or becomes deceased.

The most used version of contrary financial ‘s the household collateral transformation mortgage (HECM) in fact it is highly controlled and insured by Federal Homes Management (FHA). Its an economic equipment which enables property owners 62 and old in order to cash-out brand new security in their home without the dependence on a month-to-month financing fee. People need consistently shell out property taxation, homeowners’ insurance rates, and maintain our home.

A contrary financial are often used to purchase a new home if you’re looking so you’re able to downsize otherwise upsize. It is known as an excellent HECM for purchase. Playing with an excellent HECM to buy to find a home allows you to locate a new home without having to take on month-to-month mortgage payments. Youre nonetheless needed to shell out possessions fees, insurance rates, people HOA dues (when the applicable), and you will restoration will set you back.

In the place of traditional home loan fund, a reverse mortgage brings property owners that have winnings from their equity just like the that loan when it comes to a lump sum, fixed monthly obligations, a personal line of credit, or a combination of the 3

Just like that have a traditional financial, your house is part of your providing you meet the home mortgage requirements.

The costs away from a face-to-face financial may differ with regards to the style of financing additionally the lender, but fundamentally they is a keen origination fee, mortgage insurance costs, settlement costs, and you may appeal on loan. Such costs shall be financed included in the loan, for example the fresh debtor does not have to pay them initial.

Opposite financial financing may be used nevertheless would love. There are no restrictions precisely how the bucks can be utilized. Some traditional spends is complementing month-to-month earnings, investing in family renovations or updates, or perhaps as the an extra safety net to have unexpected costs.

Your family may still found a genetics. Adopting the residence is offered while the opposite real estate loan try paid back with the lender, one kept guarantee will go towards the heirs. There aren’t any most other possessions used to hold the financing other as compared to home.

A reverse real estate loan includes several earliest personal debt you to definitely should be satisfied after you start researching financing. They have been the next:

- Pay constant assets taxation, insurance rates, and you can one homeowners’ organization expenses, for those who fall into an HOA.

- Pay domestic repair will set you back.

- Support the domestic as your number one quarters.

- You truly must be at the least 62 yrs . old.

- You should very own your house.

- The home must be the majority of your home.

Interest rates fall and rise. If rates is lower today than just these were when you earliest grabbed your reverse mortgage or if you are interested during the swinging regarding an adjustable rates to a predetermined price, it may be really worth thinking about refinancing the loan.